Markets Hold Steady as Lower Brent Crude Prices Ease Inflation Concerns

Market Snapshot

| Asset | Price/Level | Trend |

|---|---|---|

| S&P 500 | 7,387.29 | ▲ 0.20% |

| Nasdaq Composite | 25,522.44 | ▲ 0.35% |

| Dow Jones | 52,006.35 | ▼ 0.05% |

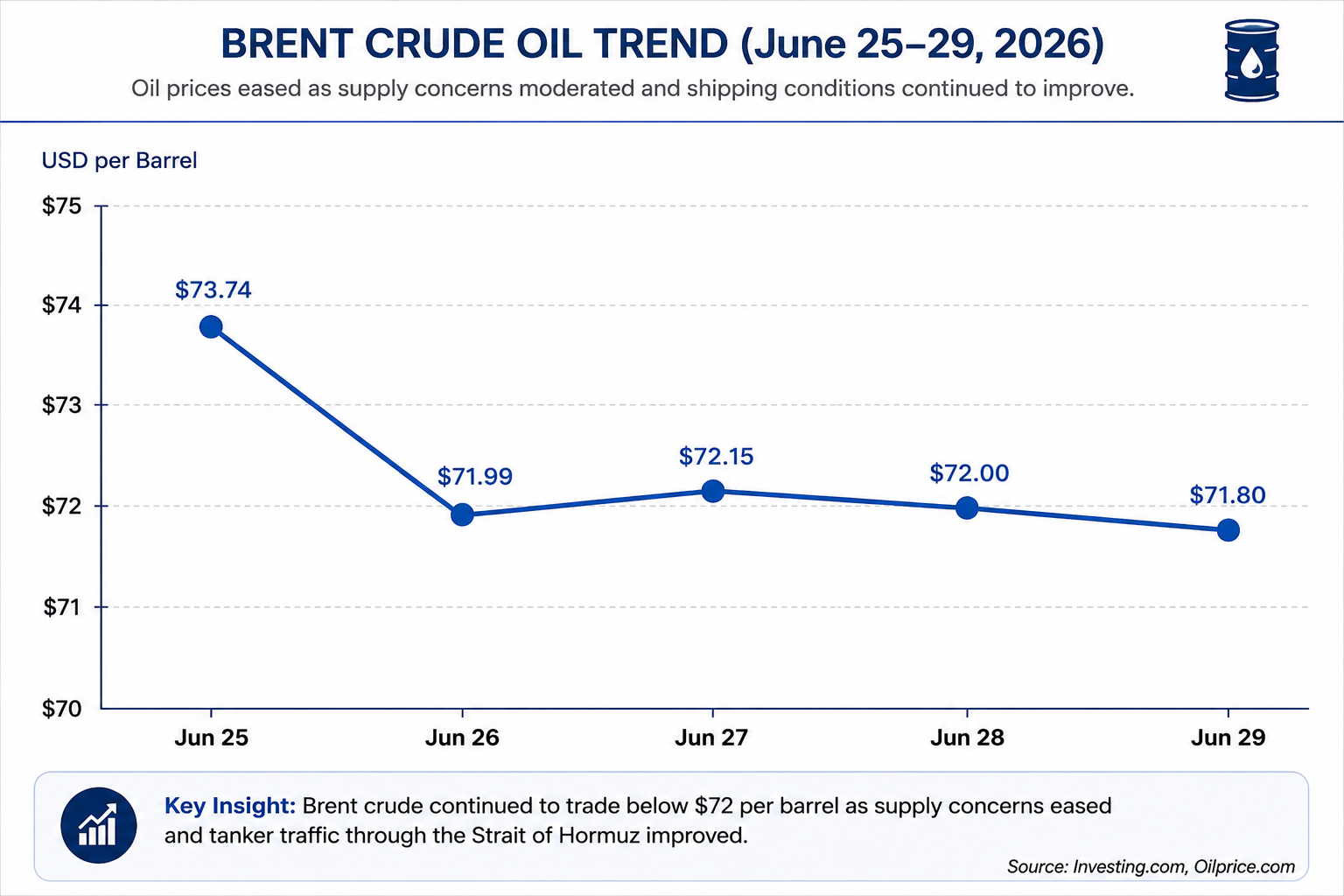

| Brent Crude Oil | $72.27/barrel | ▼ 0.28% |

| Gold | $4,094.57/oz | ▲ 0.10% |

| 10-Year Treasury Yield | 4.38% | ▼ 0.03% |

Market Summary

Global financial markets opened the week by showcasing the sheer magnitude of the ongoing tech-driven bull market, as investors continued to pour capital into equities at unprecedented valuations. Equity indexes remain at drastically elevated levels—with the S&P 500 comfortably above 7,300 and the Nasdaq surging past 25,500—underscoring the massive scale of the AI-fueled market rally. Market participants remained focused on upcoming U.S. employment data, inflation indicators, and central bank commentary, all of which could influence expectations for interest-rate policy during the second half of 2026.

Brent crude oil remained one of the primary market drivers. Prices hovered around $72.27 per barrel, extending a period of relative stability as concerns over supply disruptions in the Middle East continued to ease. Improved shipping activity through the Strait of Hormuz and expectations of steady production from major oil-exporting countries reduced fears of an immediate supply shortage. Lower energy prices were welcomed by investors as they could help moderate inflation and reduce operating costs for transportation, manufacturing, and consumer-focused businesses.

Equity markets demonstrated remarkable strength, reflecting the profound transformation brought by the AI revolution. The S&P 500 and Nasdaq Composite posted further gains, supported by relentless investor interest in artificial intelligence and technology companies. The sheer explosion in valuations across semiconductor and cloud-computing sectors highlights how AI spending has become the absolute dominant force driving corporate earnings globally.

Meanwhile, the Dow Jones Industrial Average, breaking past the 52,000 mark, traded slightly lower as investors took a breather in defensive sectors ahead of the week's major economic releases. Bond markets reflected a cautious tone amidst the euphoric stock rally, with the 10-year U.S. Treasury yield sitting at 4.38%, suggesting steady demand for government securities as investors prepared for upcoming employment and inflation data.

The U.S. dollar index strengthened modestly against major currencies, supported by expectations that the Federal Reserve will continue to adopt a data-dependent approach to monetary policy. Gold prices remained strong near $4,094 per ounce, benefiting from enduring safe-haven demand as investors look for stability alongside their massive equity portfolios.

Overall, investor sentiment remains overwhelmingly bullish on technology, driven by structural shifts in the global economy. While improving energy markets and resilient corporate earnings provide a solid foundation, traders remained vigilant ahead of several high-impact economic events that could determine near-term market direction during the coming weeks.

Market Outlook

Looking ahead, financial markets will closely monitor the U.S. Nonfarm Payrolls report, the Core PCE Inflation Index, and comments from Federal Reserve officials. Strong employment figures could reinforce expectations that interest rates will remain elevated for longer, while softer inflation data may increase optimism that policy easing could begin later this year.

Oil prices are also expected to remain a major influence on market sentiment. Continued stability in Brent crude prices below $72 per barrel would support lower inflation expectations and improve confidence across equity markets. However, any renewed geopolitical tensions affecting global energy supplies could quickly reverse recent gains and increase market volatility.

Investors are therefore expected to maintain a balanced approach, focusing on economic data, corporate earnings, and developments in energy markets before making significant portfolio adjustments.

Information Sources

- Morningstar / Dow Jones: U.S. Equity Futures and Market Snapshot

- Trading Economics: 10-Year Treasury Yield and Historical Data

- Investing.com: Brent Oil Futures and Commodity Pricing