Markets Turn Attention to Jobs Report as Rate Outlook and AI...

"Markets Turn Attention to Jobs Report as Rate Outlook and AI Volatility Shape Investor Sentiment"

Market Snapshot

| Asset | Price/Level | Trend |

|---|---|---|

| S&P 500 | 7,357.49 | Slightly Lower |

| Nasdaq Composite | Mixed | Cautious |

| Dow Jones | Slightly Higher | Positive |

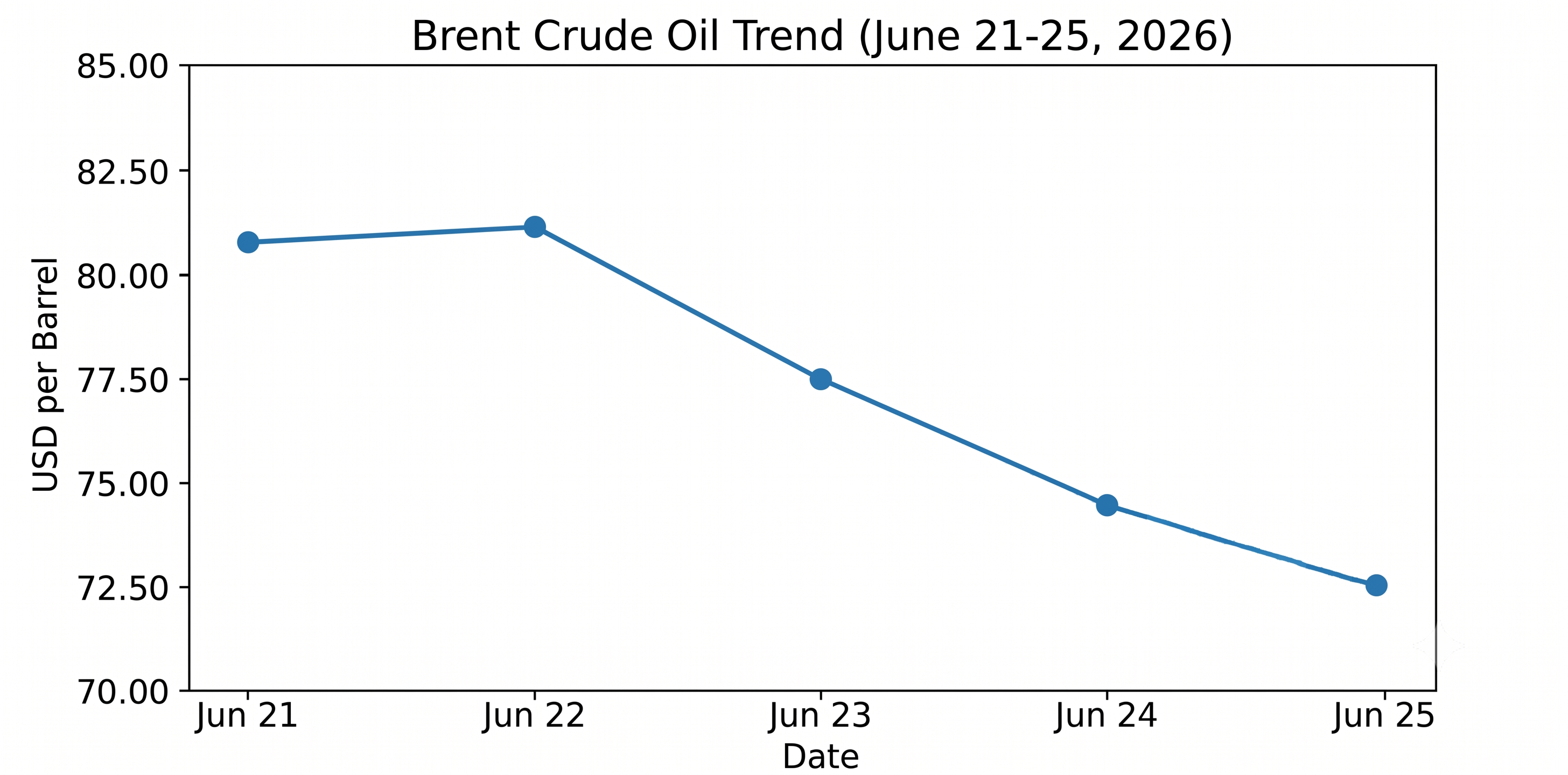

| Brent Crude Oil | $73.01/barrel | ▼ 2.99 |

| Gold | $4,030.50/oz | Stable |

| 10-Year Treasury Yield | 4.38% | Lower |

Market Trend Chart: 10-Year Treasury Yield

| Date | Yield |

|---|---|

| Jun 22 | 4.46% |

| Jun 23 | 4.43% |

| Jun 24 | 4.41% |

| Jun 25 | 4.39% |

| Jun 26 | 4.38% |

Global financial markets started the week on a positive note as investors continued to favor technology and artificial-intelligence-related stocks. U.S. equity futures moved higher amid optimism surrounding corporate earnings and continued investment in AI infrastructure. Market participants also focused on upcoming economic reports that could influence expectations for future Federal Reserve policy decisions.

Technology companies remained the primary driver of market performance, with semiconductor and cloud-computing firms attracting strong investor interest. Analysts continue to point to growing demand for artificial intelligence infrastructure and enterprise technology spending as key factors supporting earnings growth within the sector. The Nasdaq Composite outperformed broader market indexes as investors maintained confidence in long-term technology trends.

Energy markets remained active throughout the session. Brent crude oil traded above $81 per barrel as traders monitored global supply conditions and geopolitical developments. While oil prices remain below recent highs, the modest recovery reflects expectations of stable demand and cautious optimism regarding global economic activity. Rising energy prices also contributed to renewed discussion about future inflation trends and their impact on monetary policy.

Treasury yields remained elevated as investors evaluated recent comments from Federal Reserve officials. Market participants continue to assess whether inflation is moderating quickly enough to justify future policy easing. The U.S. dollar remained firm against major currencies, reflecting expectations that interest rates could remain higher for longer.

European and Asian markets delivered mixed performances, with investors balancing improving risk sentiment against concerns about slowing growth in several major economies. Despite these challenges, broader market confidence remained supported by resilient economic activity and strong performance from leading technology companies.

Market Outlook

The near-term outlook remains cautiously optimistic. Continued strength in technology stocks, stable corporate earnings, and improving energy-market conditions are supporting investor sentiment. Artificial intelligence remains one of the market's most important growth themes, with investors closely monitoring corporate spending and earnings expectations across the sector.

However, markets remain sensitive to inflation data, labor-market reports, and comments from Federal Reserve officials. Upcoming economic releases could provide important clues regarding the future path of interest rates and influence investor expectations for the remainder of the year.

Bond yields, currency markets, and commodity prices are expected to remain volatile as traders react to new economic information. Any signs of slowing inflation or weakening growth could increase expectations for future policy easing, while stronger-than-expected economic data could reinforce the case for maintaining current interest-rate levels.

For now, market sentiment remains constructive, though investors are likely to remain selective and data-driven as they evaluate opportunities during the second half of 2026.

Information Sources

- Morningstar / Dow Jones: U.S. Equity Futures and Market Snapshot

- Trading Economics: 10-Year Treasury Yield and Historical Data

- Investing.com: Brent Oil Futures and Commodity Pricing